Does money enjoy a home advantage?

Do citizens benefit by owning money that is pegged to the nation's own unit of account rather than a foreign unit of account?

Let's start by imagining a money that is not pegged to the national unit of account. Say that U.S. banking giant Wells Fargo establishes branches all over Canada. Instead of issuing chequing accounts that are pegged to the Canadian dollar, it decides that it will steal business from Canadian banks by issuing U.S. dollar-pegged chequing accounts to Canadians. Wells Fargo execs reason that the U.S. dollar is at least as stable as Canadian dollars, if not more so, and this could give their product an edge.

Further imagine that Wells Fargo is able to ensure that its U.S.-denominated money is just as liquid as that of competing Canadian money. Say that Canada's national ATM network is modified to dispense U.S. dollars to Wells Fargo cardholders. Retailers are convinced to accept U.S. dollar electronic payments, and so is Revenue Canada, the national tax authority. The upshot is that within Canadian borders, a U.S. dollar can do anything that a Canadian dollars can. Any Canadian in need of liquidity will be entirely indifferent between regular C$ deposits and Wells Fargo US$ deposits.

Let's also assume that shifting funds between U.S. and Canadian dollars is free, so Canadians who are paid in one unit have no compunctions about exchanging into the other. Apps and other technologies remove all inconveniences of calculating exchange rates. Finally, Wells Fargo's U.S. dollars are FDIC-insured and its Canadian branches have access to the Fed's discount window, making them just as safe as Canadian dollars.

This leaves just one difference between the two types of money; Canadian dollars are the unit of account. This means that retailers set prices in Canadian dollars, not U.S. dollars. Will this feature have any influence on whether Canadian consumers choose to open an account with Wells Fargo or stay with their existing bank?

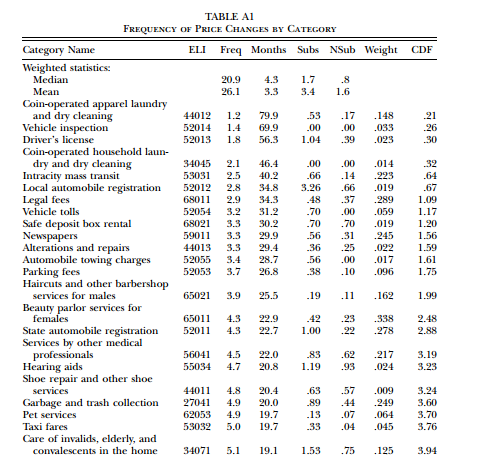

Consumer prices are peculiar because, unlike asset prices, they stay constant for long spells of time. When examining the frequency of price changes for 350 categories of goods and services, Bils and Klenow found that prices tend to stay fixed for 4.3 months before they are updated. Coin-operated laundry prices exhibited price spells of 79.9 months, driver's license fees 56.3 months, and newspapers 29.9 months (see below). On the short end of the spectrum, the price spell for gas is just 0.6 months, eggs 1 month, and women's suits 1.6 months.

|

| Source: Bils & Klenow |

One reason for this stickiness is that retailers are said to have made an "invisible handshake" with consumers that requires them to avoid raising prices when demand suddenly increases. Retailers bind themselves to this implicit contract because they do not want their loyal customers to view them as being unfair, spitefully bolting to the competition when prices are adjusted. Customers may prefer stable nominal prices because these allow them to carefully match their daily and weekly spending plans with the money currently available in their accounts. Put differently, if you've got $100 in your account, and the set of retailers at which you shop have promised not to budge on pricing for a few weeks, you can determine ahead of time what bundles of goods you can afford. Without the sticky price "handshake," you're in the dark.

So money that is denominated in the unit of account comes with a major ancillary benefit. In Canada's case, the nation's retailers have agreed to offer Canadian dollar owners a convenient planning mechanism, much like a day planner or personal organizer. This mechanism provides anyone who owns Canadian dollars around 4.3 months of uncertainty alleviation within national borders.

Whereas Canadian sticker prices are characterized by long price spells, the U.S. dollar prices faced by Wells Fargo's Canadian customers will fluctuate by the second. To see why, consider that when a customer wants to pay in U.S. dollars, they will have to indicate their preference at the checkout counter. The retailer inputs the Canadian dollar sticker price of the good, multiplies it by the USD/CAD exchange rate, and arrives at the U.S. dollar price. The foreign exchange market is a 24 hour "flex-priced" market, so the exchange rate--and thus the U.S. dollar sticker price of goods--will always be fluctuating.

Wells Fargo money will therefore not be able to provide the same set of uncertainty-minimizing features that Canadian money provides. Anyone who holds, say, $100 U.S. dollars in their account cannot know ahead of time how much stuff they'll be able to buy over the ensuing three or four days. An equivalent C$100 provides near certainty. Lacking this nice property, Wells Fargo money faces significant headwinds at the outset.

This explains a point I was trying to make in my previous post on bitcoin. Bitcoin's battle to gain general acceptance will be a harder one to win than Wells Fargo's in Canada because the price of bitcoin is so much more volatile than U.S. dollars. Even if bitcoin's price eventually stabilizes so that it is just about as volatile as the U.S. dollar, it must still overcome the same unit-of-account hurdle as Wells Fargo i.e. neither can mimic the 'day planner' properties of the Canadian dollar. I don't think is an easy problem to overcome.

PS: Another complicating factor is product returns. If someone doesn't like the t-shirt they bought, and they paid in bitcoin, refunds are usually issued in U.S. dollars at the bitcoin-to-dollar conversion rates in play at the time of the transaction. So it's possible to make or lose bitcoin on refunds. For bitcoin owners, this adds an extra degree of uncertainty. Pay in dollars and you can be certain you'll get the exact same nominal amount back if the product is unsatisfactory. Pay in bitcoin and who knows what the amount of bitcoin you'll be refunded.

0 Response to "Does money enjoy a home advantage?"

Posting Komentar