Alberta Prosperity Certificates and a Greek parallel currency

This post is about the Alberta Prosperity Certificate, one of the world's stranger monetary experiments. Issued in late 1936 and early 1937 by the newly-elected Alberta government, these monetary instruments are the largest-scale example of Silvio Gesell's "shrinking money," or stamp scrip, in action. Gesell, a German business man and self taught economist, had written a treatise in 1891 in which he described a currency that depreciated in value, thus preventing hoarding and encouraging spending.

To make this more interesting, let's jump forward in time. In 2014, Greece's Finance Minister Yanis Varoufakis wrote a blog post that described a new Greek financial instrument that could be used to make payments while circulating in parallel with the already-existing euro. Varoufakis's post, combined with constant rumors that Greece may be planning to issue its own parallel currency in order to make internal payments,* means that a revisitation of Alberta's early dalliance with scrip, which circulated concurrently with Canadian dollars, is more relevant than ever. The attempt by Albertan authorities to issue scrip 80 years ago would end in failure; most of the paper refused to stay in circulation. Understanding why this happened provides some insights into what sorts of conditions might promote the success of a Greek parallel currency—or its downfall.

Virginius Frank Coe

The best source on Prosperity Certificates is a 1938 survey by Virginius Frank Coe, an American economist who visited Alberta in August 1937, five months after the program had been abandoned. Coe's life is interesting enough to deserve its own tangent. An economist educated at the University of Chicago, Coe would go on to hold a number of important positions in various U.S. government institutions both during and after World War II, including monetary research director at the Treasury Department. This brought him into the orbit of Harry Dexter White, then the Assistant Secretary of the Treasury and the architect of the Bretton Woods agreements. Coe himself was a representative at Bretton Woods and would go on to become secretary of the International Monetary Fund in 1946, nine years after having written his Prosperity Certificate paper.

Readers of Benn Steil's The Battle of Bretton Woods will know that much of the evidence incriminates Harry Dexter White as spying for the Soviets, an accusation White himself denied. The same sources who named White as a Soviet agent also fingered Coe, and in 1952 Coe was forced to resign from his post at the IMF. He would appear in front of the McCarran Committee later that year, pleading the fifth in response to all questions posed to him, and would later face Senator Joseph McCarthy. His passport revoked, and unable to find work in the U.S., Coe headed to China to serve as an adviser to Mao until his death in 1980.

Coe's Prosperity Certificate paper betrays the author as someone with a strong interest in alternative monetary systems. While we can't know for sure if his interest in alternative systems extended as far as being a Soviet mole, we shouldn't let this possibility detract from what is otherwise an excellent account of this early Canadian monetary experiment.

Alberta and Social Credit

Coe describes an Alberta electorate that is facing the same economic backdrop as Greece's voters did prior to the recent election of Syriza. Just as Greeks had endured seven years of famine prior to the 2015 election, Albertans going into the 1935 election had been beset by seven years of distress associated with low farm prices and bad crop yields. The incumbent United Farmers of Alberta government was not willing to implement the more drastic policies that the Albertan electorate demanded, says Coe. Into the void stepped William Aberhart, a pastor and newly-recruited believer in the tenets of Social Credit. Dreamt up by British engineer C.H. Douglas, the idea behind Social Credit was to create a more equal society by augmenting consumers' purchasing power via the payment of a national dividend. Aberhart formed the Alberta Social Credit party in 1935 and won the election a few months later. In electing Syriza, the Greeks, like the Albertans before them, have entrusted their future to a party of political novices.

Reading Coe, one gets the sense that the Aberhart government stumbled into Prosperity Certificates rather than purposefully selecting them as a policy. Gesell's dated stamp scrip was a rival monetary reform to Social Credit, not a complement. Why turn to a non-Social Credit policy? It seems that several months after coming to power, the new Social Credit government was already splintering as one faction had grown impatient with Aberhart's inability to implement economic changes. Coe, speculating that the decision to implement dated stamp money was a token gesture to demonstrate forward momentum and heal internal rifts, says that "any one of a number of plans would have done as well." If a non-Social Credit monetary scheme such as Gesell money were to fail, at least a Social Credit policy option still had a kick at the can. The implication that the government didn't put much thought into the design of the certificates finds some confirmation in the fact that the Free-Economy League, an organization formed by Gesell, published a criticism of the Alberta government's procedure for creating Prosperity Certificates and predicted their failure.

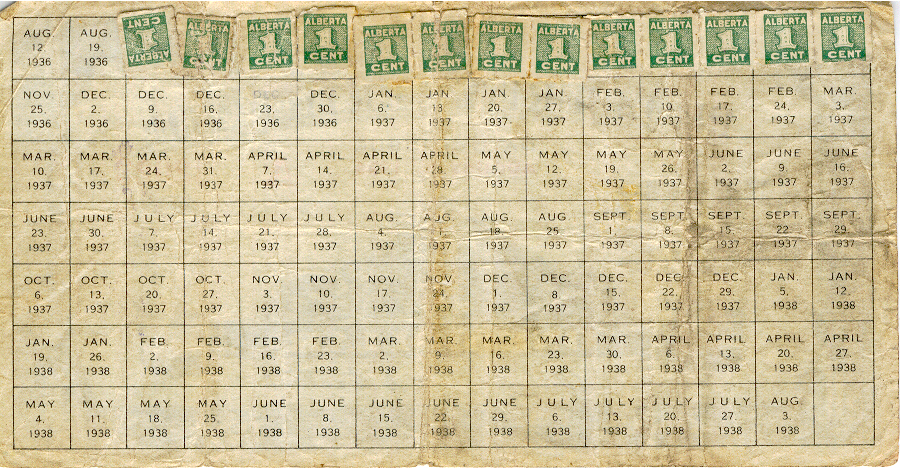

How the certificates worked

Here's how Alberta's stamp scrip worked. In early August 1936, when the program debuted, an unemployed Albertan was paid, say, a $1 certificate for each $1 worth of road maintenance work rendered. This certificate was to be redeemed by the Alberta government two years hence, or in August 1938, for $1 in Canadian dollars. However, redemption required that the certificate have 104 stamps affixed to it (see figure above). Each week during that two year period, the owner of the certificate was to buy a government stamp for 1 cent from an approved stamp dealer and glue it to the note.

The necessity of buying stamps created a fairly onerous fee on cash holdings. As such, any laborer who received the scrip from the government was unlikely to hoard it, preferring instead to spend it on, say at a retailer, who in turn would only accept scrip as payment for goods and services if the correct number of stamps has been affixed. In order to avoid the cost of buying the next weekly stamp in order to keep the scrip current, the retailer themselves would quickly offload it to their suppliers and so on.

The 1 cent stamp fee was collected by the Alberta government and held as a reserve for redemption in two years. With 104 cents being collected over each $1 certificate's life time, this meant that the scheme was entirely self financing. The extra four cents represented a profit to the government.

Failure

We know that the Prosperity Certificate scheme didn't work. The certificates began to be paid to unemployed Albertans in August 1936 for roadwork rendered in July. According to Coe, the maximum amount of outstanding certificates in circulation in August and early September was $239,391 (around $9 million in current dollars). However, by mid-September 1937, just one month after the program's debut, over 60% of the certificates outstanding, or $144,280 out of $239,391, had ceased to circulate.

Where had they gone? The government now held them. The reason for this development was a last minute decision by Aberhart to offer monthly redemption of certificates at par in Dominion currency (i.e. $1 in certificates for $1 in Canadian bills). This short-circuited the original two-year life of the certificates. Rather than continuing to pass the scrip along to the next Albertan, Albertans leapt at the government's offer and converted en masse when the first redemption date presented itself in early September.

In the end, the government might as well have paid for work rendered using Canadian dollars, since the net effect of paying in either Certificates or Canadian dollars was the same. As Coe says, "the dated stamp scrip was in the end little more than a small nuisance." Subsequent issues of scrip were small relative to the original August 1936 issue and the government officially ended the program in April 1937.

"The problem of the wholesalers"

In the planning stages of the program, government officials ran into what Coe refers to as the "problem of the wholesaler." The first to receive the certificates would be farmers on relief, who in turn would make payments to retailers. The payments by retailers would primarily flow to Albertan wholesalers whose dominant payments were to manufacturers and others outside the province. However, those outside the province would not accept Prosperity Certificates, requiring instead hard currency, or Canadian dollars. The Albertan wholesaler would be left holding the bag, so to say, having acquired the entire issue of Prosperity Certificates with no outlet. According to Coe, wholesalers and large retailers were vocal in their opposition to the plan, which they expressed through trade associations and in the press.

One way of solving the wholesalers' problem would have been to establish an exchange market such that wholesalers could sell certificates in order to buy the necessary hard currency and thus fund out-of-Province imports. Banks would normally be an important party to the creation of such a market. Irving Fisher, who wrote a book on stamp scrip, entitled one paragraph "Have at Least one Bank." But the banks who operated in Alberta refused to participate in the Prosperity Certificate scheme—no wonder given that one of the Social Credit party's planks advocated the removal of the "banking monopoly" on the issuance of credit. The tenets of Social Credit thus interfered with the execution of Gesell money, impeding the latter's success.

Even if such a market were to be created, chances are that it would have priced the Certificates at a large discount to Canadian dollars given the onerous fee on certificates relative to Canadian notes and the inferior credit of their issuer. After all, by then the Alberta government had defaulted on its international obligations whereas the Federal government's credit was still good. Such a discount would have been at odds with the Alberta government's policy of using a dollar's worth of certificates to buy one Canadian dollar's worth of labour. If the certificates were trading at 69 cents on the dollar in the wholesale market, workers paid in scrip would be loath to accept them at face value, for if they did, they would probably have problems passing them off at retailers for that amount.

In the end, the government's solution to the problem of the wholesalers was to allow wholesalers (and even retailers) to benefit from free monthly redemption at par. As I noted earlier, this resulted in most of the certificates being returned for redemption just a few weeks after having been issued.** Rather than bad money driving out the good, a garbled version of Gresham's Law had taken hold in Alberta, which Coe describes thusly: "Bad money obviously does not drive out good money when the government is willing to redeem the bad money in good money."

This garbled version of Gresham's law is a phenomenon I've described before to explain a number of monetary puzzles including the failure of the Susan B. Anthony dollar, the European Target2 bank runs of 2011-12, the proliferation of credit cards, and the zero-lower bound problem. See here and here.

What about Greece?

Alberta in 1936 and Greece in 2015 are in similar situations. Both are non-currency issuers within a larger monetary zone, in Alberta's case the Canadian dollar zone and in Greece's case the Eurozone. Both have awful credit. Neither is part of a larger fiscal union. In Greece's case, the mechanism hasn't yet been created whereas in Alberta's case, the Social Credit party was at such odds with the Federal government and the rest of Canada that it could not expect much help.

I'd argue that anyone planning to introduce a Greek parallel currency to circulate alongside euros faces the same problem that Alberta faced; the so-called problem of the wholesalers. If the Greek government starts to pay employees and contractors in Greek parallel IOUs denominated in euros, and employees buy stuff at stores with those IOUs, and stores purchase inventory from wholesalers, these wholesalers will need a mechanism to offload their parallel note surpluses in order to get euros to buy foreign imports. The IOUs can either find their own price, in which case they will most likely trade at a large and varying discount to euros, or the Greek government can offer one-to-one convertibility. They can do this by either redeeming IOUs directly for euros or allowing one euro worth of taxes to be paid with an equivalent number of IOUs.

Neither solution is ideal. If the IOUs trade at a variable discount to euros, then their ability to serve as a competing medium of exchange will suffer. People always prefer to trade using the medium in which a nation's prices are expressed, or, put differently, the medium which functions as a unit of account. For example, people see benefit in the fact that one euro will always discharge a euro's worth of Greek debt or a buy a euro's worth of Greek olive oil. But as long as Greek IOUs trade at a varying discount to euros, it is impossible to know ahead of time how many IOUs will discharge a euro's worth of debt or buy a euro's worth of oil, given that the euro will surely remain Greece's unit of account. This would hinder the IOU's ability to function as a currency. The fact that people prefer to accept stable exchange media in trade to unstable media is one of the reasons that bitcoin hasn't caught on.

So rather than serving as a competing medium of exchange, the parallel IOUs will probably function as illiquid and highly risky speculative fixed income securities. In order to compensate recipients of IOUs for this lack of liquidity, the Greek government will have to issue the IOUs at a larger discount to par than they would for an otherwise liquid equivalent, thus increasing the government's financing costs.

This lack of liquidity militates against one of the key selling points of a Greek parallel unit, which is to finance the government by displacing some of the existing circulating medium of exchange, euros, from citizens' wallets. Preferably, unwanted euros would trickle back to the European Central Bank to be cancelled, reducing the ECB's seigniorage but augmenting the seigniorage of the Greek state as Greek IOUs rush in to fill the void. However, if the new Greek parallel unit cannot compete with the euro's liquidity, then there will be very little 'space' for Greek IOUs to occupy in Greek portfolios, and little relief for beleaguered government finances.

If the Greek government tries to promote the liquidity of its parallel currency by having the units trade at a fixed one-to-one rate with euros, then the same garbled version of Gresham's Law that took hold in Alberta would overwhelm Greece. In Coe's words, the Syriza government's willingness to buy bad money, or parallel currency units, from the public with good money, or euros, will promote mass conversion into euros and thereby drive all the bad money from circulation. Greek parallel units will cease to exist.***

In sum, anyone planning a Greek parallel currency faces a conundrum. In order to pay its bills the government can do little more than introduce a volatile asset that trades at varying discount to euros. This asset's volatility and relative illiquidity won't make it very popular with its recipients. An attempt to render that asset more acceptable in trade by setting a one-to-one conversion rate to the euro will result in a short-circuiting of the scheme as everyone races to redeem IOUs. The issuance of parallel currencies seems like a hard battle to win.

*There are a number of plans including that of Biagio Bossone & Marco Cattaneo, Thomas Mayer, and Robert Paranteau

** Compounding the problem was that redemption at face value put a premium upon redemption, says Coe. "The holder who redeemed received face value; the person who did not redeem ran the risk of losing 1 per cent of the face value if he failed to pass the certificates within the next few days, and more for longer periods. This premium placed upon redemption could only have been eliminated by redeeming the certificates at a discount of more than 1 per cent-say, 2 or 3 per cent." So the government accidentally created an even greater incentive for certificate owners to redeem.

*** This is particularly damaging in Greece's case at will result in a perpetual draw down in the state's euro balances. These reserves are vital since the Greek government needs to service its (existing or renegotiated) Euro debts to the IMF and pay external suppliers, and can only do so with hard currency.

0 Response to "Alberta Prosperity Certificates and a Greek parallel currency"

Posting Komentar